Simplifying Homeownership

See EXACTLY How Much Home You Qualify For Today!

Simplifying Homeownership

See EXACTLY How Much Home You Qualify For Today!

Learning Center

How to Read a Loan Estimate — And Why Section A Could Save You Thousands

Within three business days of submitting a mortgage application, your lender is legally required to hand you a document called a Loan Estimate. It is a standardized, three-page form mandated by the Consumer Financial Protection Bureau (CFPB), and it is one of the most important pieces of paper you will receive during the homebuying process.

Most people glance at it, feel overwhelmed, and set it aside.

That is a costly mistake — because buried inside this document is everything you need to know about what your lender is actually charging you, how much your loan will truly cost, and whether you are getting a fair deal or leaving thousands of dollars on the table.

This guide will walk you through the Loan Estimate section by section, with special attention to Section A: Origination Charges — the part of the document that most directly reveals whether working with a mortgage broker versus a retail bank could save you significant money.

What Is a Loan Estimate?

The Loan Estimate (often abbreviated LE) replaced the old Good Faith Estimate in 2015 as part of the TRID rule. It is a standardized, government-required form that every lender must provide in the same format — which means you can use it to compare offers apples-to-apples across multiple lenders.

- Your loan amount, interest rate, and monthly payment

- Whether your rate and costs can change before closing

- An itemized breakdown of every closing cost

- How much cash you will need at the closing table

- Projected payments over the life of the loan

You are not committed to anything by receiving a Loan Estimate. It is your right to shop around and compare estimates from multiple lenders before choosing one.

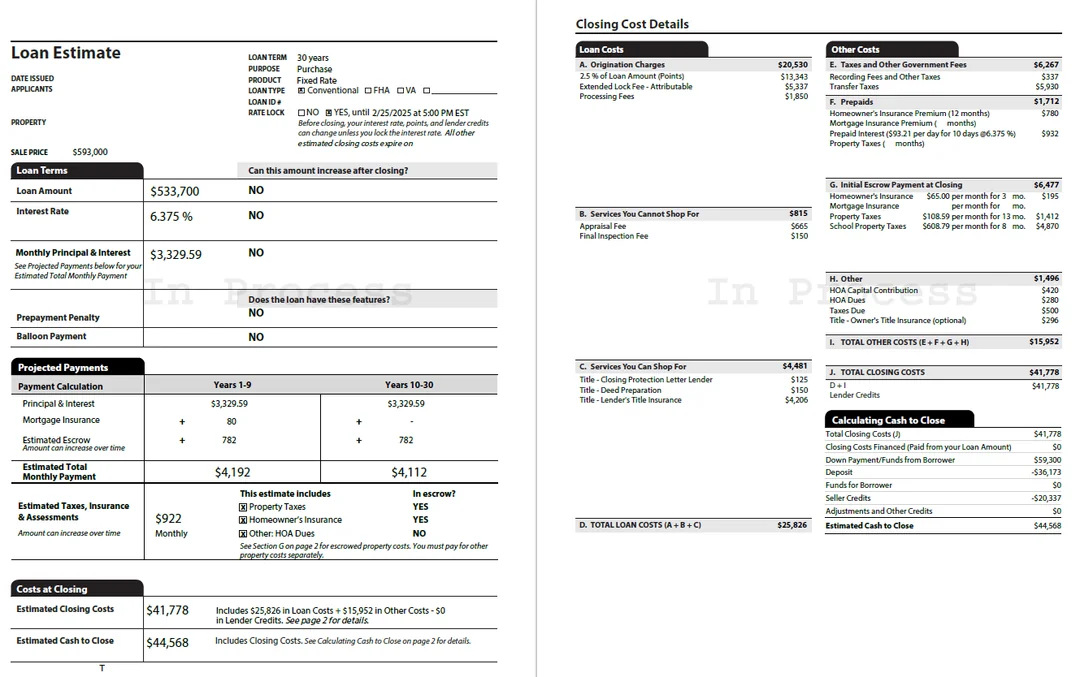

A Real Loan Estimate: What It Actually Looks Like

Below is an example of a real Loan Estimate. Take a moment to look at it — then we will walk through each section together.

Sample Loan Estimate — the standardized form every lender must provide within 3 business days of application

Key details from this example LE: $593,000 sale price · $533,700 loan amount · 6.375% interest rate · $3,329.59 monthly P&I · 30-year fixed conventional · Estimated cash to close: $44,568

Page 1: Loan Terms and Projected Payments

The first page contains the headline numbers. The Loan Terms box answers the three questions buyers care most about: What is my loan amount? What is my interest rate? What is my monthly payment? On a fixed-rate loan, the answer to whether any of these can increase after closing should be NO — your rate and payment are locked for life.

The Projected Payments table shows your total monthly payment broken down across the life of the loan — including Principal and Interest, Mortgage Insurance if applicable, and Estimated Escrow. In this example, total estimated monthly payment is $4,192 in years 1–9, dropping to $4,112 after mortgage insurance falls off at year 9.

At the bottom of page 1: Estimated Closing Costs ($41,778) and Estimated Cash to Close ($44,568). These are the summary totals — the details are all on page 2.

Page 2: Closing Cost Details — Where the Real Story Is

Page 2 divides into two major buckets: Loan Costs (Sections A, B, C, D) and Other Costs (Sections E, F, G, H, I). The Other Costs sections — government recording fees, property taxes, homeowner's insurance, HOA dues — are largely fixed regardless of which lender you choose. The place where lenders differ most dramatically is Section A.

The key insight: Sections E through H are essentially identical no matter who you borrow from. Section A is where your lender either earns your trust — or takes advantage of your lack of information.

Section A: Origination Charges — The Most Important Number on the Page

Section A shows what the lender is charging you to originate the loan. It is pure lender profit and overhead — and it is 100% negotiable and variable between lenders. In our example, Section A totals $20,530 on a $533,700 loan.

Points are prepaid interest. One point = 1% of the loan amount. They buy your rate down — but only make financial sense if you stay in the home long enough to recoup the upfront cost through monthly savings. At retail banks, points often appear as pure profit built into the rate structure. Wholesale lenders — the ones mortgage brokers access — typically charge zero to minimal origination because they are not funding a retail branch network.

Extended Lock Fees reflect the cost of holding a rate for longer than the standard 30–45 day window, common on new construction. The $5,337 here is a lock cost, not pure profit.

Processing Fees cover the lender's cost to review your file and prepare it for underwriting. These vary significantly across lenders.

Retail Bank vs. Mortgage Broker: Why Section A Tells the Whole Story

Here is what most homebuyers never learn — and it can mean thousands of dollars at the closing table.

The Wholesale Rate Advantage — $500,000 Loan Example

Illustrative example. HMDA data shows borrowers using mortgage brokers save an average of $10,000+ over the life of their loan.

The Rest of the Closing Cost Sections

- Section B — Cannot Shop ($815): Appraisal and final inspection. Third-party costs — vendors are assigned, not chosen.

- Section C — Can Shop ($4,481): Title insurance and title services. You can shop these and find meaningful savings, especially in Washington State.

- Section E — Government Fees ($6,267): Recording fees and transfer taxes set by county and state — not negotiable.

- Section F — Prepaids ($1,712): Homeowner's insurance and prepaid interest. Real expenses, not lender profit.

- Section G — Initial Escrow ($6,477): Your upfront escrow deposit for taxes and insurance. This money is yours — held to cover future bills.

- Section H — Other ($1,496): HOA capital contribution, HOA dues, taxes due, and optional owner's title insurance.

How to Use the Loan Estimate to Compare Lenders

- Apply with at least two lenders — or work with a broker who shops multiple wholesale lenders simultaneously.

- Compare Section A first. Lower is better. A broker with wholesale access will almost always win this comparison.

- Compare rate and APR. The APR factors in both rate and fees — a better comparison than rate alone.

- Check the page 3 summary. The "In 5 Years" and "APR" fields give you a quick total cost view.

- Ask about lender credits. A slightly higher rate in exchange for covering closing costs can save you significant cash upfront.

Pro Tip: A slightly lower rate with high origination fees may cost you more than a slightly higher rate with zero origination charges — especially if you are not staying in the home 10+ years. Always evaluate rate and Section A together.

Bottom Line: The Loan Estimate Is Your Leverage

Most homebuyers accept the first Loan Estimate they receive without question. The ones who shop around — or who start with a mortgage broker who does the shopping for them — consistently end up with better rates, lower fees, and thousands more in their pockets at the closing table and over the life of the loan.

The difference almost always shows up in Section A.

Want a Second Opinion on Your Loan Estimate?

If you have already received a Loan Estimate — or are about to start the process — I am happy to review it and show you how it compares to wholesale pricing for your scenario.

Said Hamood · NMLS #1827048 · Barrett Financial Group

Serving Washington State homebuyers · Wholesale rates across 50+ lenders

Loan Estimate example shown is for educational illustration purposes only. Actual loan terms, rates, and costs vary based on credit profile, loan amount, property type, and market conditions. This is not a commitment to lend. Said Hamood, NMLS #1827048, Barrett Financial Group, LLC. Licensed in Washington State. Equal Housing Lender.

What is the first step in buying a home?

The first step is understanding your budget and getting pre-approved for a mortgage. This helps you know what you can afford and shows sellers that you're a serious buyer. I can guide you through this process to make sure you're prepared and confident.

How much money do I need for a down payment?

Down payments typically range from 3% to 20% of the home’s purchase price, depending on the type of loan you qualify for. There are also programs for first-time homebuyers that may offer down payment assistance. I can help you explore your options.

What does pre-approval mean, and why is it important?

Pre-approval means a lender has evaluated your financial information and determined the loan amount you're eligible for. It’s crucial because it gives you a clear idea of your budget, helps you compete with other buyers, and speeds up the closing process once you find a home.

What types of loans are available for first-time homebuyers?

There are several loan options, including FHA loans, USDA loans, and conventional loans. The best option for you depends on factors like your credit score, income, and the location of the home. I can help you compare the options and choose the best one for your situation.

How do I know if I qualify for a mortgage?

Lenders look at factors like your credit score, income, debt-to-income ratio, and the amount of money you have for a down payment. The good news is that I work with a range of clients, from those with perfect credit to first-time buyers, to help you find the right path to homeownership.

What are closing costs, and how much should I expect to pay?

Closing costs usually range from 2% to 5% of the home's purchase price and cover fees like appraisals, inspections, and lender charges. I’ll help you understand all the costs involved so there are no surprises at the end of the process.

Can I get a mortgage if I have student loans or other debt?

Yes! Many buyers with student loans or other forms of debt still qualify for a mortgage. Lenders look at your overall financial picture, including your income and debt-to-income ratio. Let’s talk through your situation, and I’ll help you find the best solution.

How long does the home buying process take?

The process typically takes about 21 to 45 days from the time you make an offer to closing. However, this can vary depending on factors like inspections, appraisals, and the lender's processing time. I’ll keep you updated every step of the way so you know what to expect.

What happens if my offer on a home is accepted?

Once your offer is accepted, the next steps include signing a purchase agreement, scheduling inspections, and finalizing your mortgage application. From there, the lender will process your loan, and we'll work together to ensure everything is in place for a smooth closing.

How do I know if I’m ready to buy a home?

If you’re financially stable, have a reliable income, and can afford a down payment and monthly mortgage payments, you might be ready. I’ll help you assess your financial readiness and guide you through the process to ensure you’re making the best decision for your future.

What is an FHA loan?

An FHA loan is a government-backed mortgage designed to help first-time homebuyers and those with less-than-perfect credit. It typically requires a lower down payment (as low as 3.5%) and has more flexible credit requirements, making it an excellent option for those who might not qualify for conventional loans.

What is a VA loan, and who qualifies?

A VA loan is a mortgage loan backed by the U.S. Department of Veterans Affairs, designed for military service members, veterans, and certain members of the National Guard and Reserves. It typically requires no down payment or private mortgage insurance (PMI), making it a great option for those who qualify.

What is a USDA loan?

A USDA loan is a government-backed mortgage offered to homebuyers in rural and suburban areas. It requires no down payment and offers competitive interest rates. To qualify, buyers need to meet income and property location requirements, making it a great option for those looking to buy in rural areas.

What is a conventional loan?

A conventional loan is a mortgage that is not insured or backed by the federal government. These loans usually require a higher credit score and a larger down payment than FHA loans, but they come with more flexible terms and potentially lower mortgage insurance costs if you put down at least 20%.

What is a jumbo loan?

A jumbo loan is a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These loans are typically used for luxury or high-value homes and require stricter credit and income qualifications. They also tend to have higher interest rates due to the larger loan amounts.

What is a fixed-rate mortgage?

A fixed-rate mortgage is a loan with an interest rate that stays the same throughout the life of the loan, typically 15, 20, or 30 years. This provides stability and predictable monthly payments, making it a popular choice for many homebuyers.

What is an adjustable-rate mortgage (ARM)?

An adjustable-rate mortgage (ARM) is a type of loan where the interest rate can change periodically based on market conditions. ARMs typically start with lower rates for the first few years and then adjust. While this can offer lower initial payments, it comes with more risk as rates can increase over time.

What is a renovation loan?

A renovation loan, like the FHA 203(k) loan, allows you to finance both the purchase of a home and the cost of repairs or renovations in one loan. This can be a great option if you want to buy a fixer-upper and make improvements to it, as it allows you to finance the project upfront.

"I educate first-time homebuyers so they can make informed decisions"

Said Hamood - Seattle Mortgage Broker - NMLS#1827048

Said Hamood | NMLS #1827048 | Barrett Financial Group, L.L.C. | NMLS #181106 | 275 E Rivulon Blvd, Suite 200, Gilbert, AZ 85297 | TX view complaint policy at www.barrettfinancial.com/texas-complaint | WA MB-181106 | Equal Housing Opportunity | This is not a commitment to lend. *All loans are subject to credit approval. | mlsconsumeraccess.org/EntityDetails.aspx/COMPANY/181106