Simplifying Homeownership

See EXACTLY How Much Home You Qualify For Today!

Simplifying Homeownership

See EXACTLY How Much Home You Qualify For Today!

Learning Center

Decoding the Latest Inflation Data: What It Means for Loans and Rates

Hey there, fellow borrowers and investors! Said Hamood here, your friendly neighborhood loan officer in the beautiful state of Washington. Today, I want to break down the recent inflation data that just dropped on us and what it means for all things loans and interest rates.

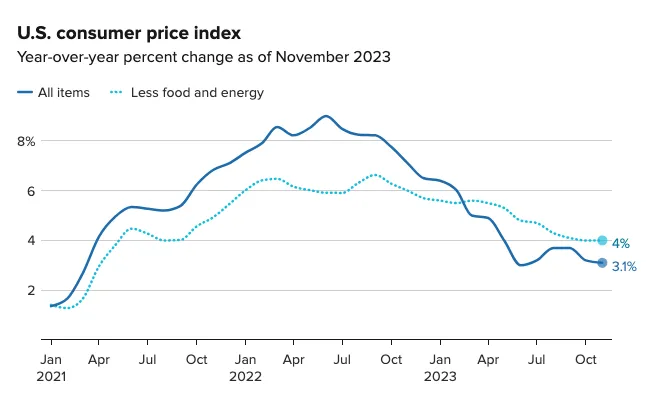

Inflation in Check: Just as the Fed Ordered

So, the latest scoop is that the consumer price index (CPI) in November increased by a modest 0.1%, bringing the yearly rate to 3.1%. Now, if you're wondering, "Is that good or bad?" - well, it's pretty much right where the Federal Reserve had its eyes set. The market was expecting no gain and a yearly rate of 3.1%, and that's precisely what we got.

Core CPI: The Real MVP

Now, let's talk about the real star of the show – the core CPI. Stripping out the volatile food and energy prices, the core CPI rose by 0.3% on the month and 4% from a year ago. Why does this matter? Because it's holding steady and coming down just as expected, indicating some positive trends in the broader economy.

What Caught My Eye as a Loan Officer:

As someone knee-deep in the loan game, I've got my radar finely tuned to anything that could sway interest rates. Here's my take:

Energy Prices Doing the Heavy Lifting: A 2.3% decrease in energy prices helped keep inflation in check. Gasoline fell by 6%, and fuel oil was down 2.7%. Good news for our wallets and the overall inflation picture.

Shelter Prices Holding Strong: Shelter prices, a significant part of the CPI, increased by 0.4% on the month and were up 6.5% on a 12-month basis. That's something to keep an eye on, especially if you're in the real estate game.

Fed Meeting on the Horizon: With the Fed meeting on the horizon, the report suggests a pause in rate hikes. The expectation is that rate cuts might be on the table in 2024. This aligns with what the market is anticipating.

My Take as a Loan Officer in Washington State:

In our neck of the woods, this data suggests a potential stabilizing of interest rates, which is generally good news for those in the market for a loan. However, we're not out of the woods yet. With the Fed meeting just around the corner, it's essential to keep a watchful eye on the signals they send about future rate movements.

Closing Thoughts: So, there you have it – a breakdown of the recent inflation data from your friendly neighborhood loan officer. As always, stay informed, stay engaged, and feel free to drop your thoughts in the comments. Let's navigate these financial waters together.

Cheers to financial wisdom and savvy borrowing!

Connect with me on social media for more updates and discussions.

What is the first step in buying a home?

The first step is understanding your budget and getting pre-approved for a mortgage. This helps you know what you can afford and shows sellers that you're a serious buyer. I can guide you through this process to make sure you're prepared and confident.

How much money do I need for a down payment?

Down payments typically range from 3% to 20% of the home’s purchase price, depending on the type of loan you qualify for. There are also programs for first-time homebuyers that may offer down payment assistance. I can help you explore your options.

What does pre-approval mean, and why is it important?

Pre-approval means a lender has evaluated your financial information and determined the loan amount you're eligible for. It’s crucial because it gives you a clear idea of your budget, helps you compete with other buyers, and speeds up the closing process once you find a home.

What types of loans are available for first-time homebuyers?

There are several loan options, including FHA loans, USDA loans, and conventional loans. The best option for you depends on factors like your credit score, income, and the location of the home. I can help you compare the options and choose the best one for your situation.

How do I know if I qualify for a mortgage?

Lenders look at factors like your credit score, income, debt-to-income ratio, and the amount of money you have for a down payment. The good news is that I work with a range of clients, from those with perfect credit to first-time buyers, to help you find the right path to homeownership.

What are closing costs, and how much should I expect to pay?

Closing costs usually range from 2% to 5% of the home's purchase price and cover fees like appraisals, inspections, and lender charges. I’ll help you understand all the costs involved so there are no surprises at the end of the process.

Can I get a mortgage if I have student loans or other debt?

Yes! Many buyers with student loans or other forms of debt still qualify for a mortgage. Lenders look at your overall financial picture, including your income and debt-to-income ratio. Let’s talk through your situation, and I’ll help you find the best solution.

How long does the home buying process take?

The process typically takes about 21 to 45 days from the time you make an offer to closing. However, this can vary depending on factors like inspections, appraisals, and the lender's processing time. I’ll keep you updated every step of the way so you know what to expect.

What happens if my offer on a home is accepted?

Once your offer is accepted, the next steps include signing a purchase agreement, scheduling inspections, and finalizing your mortgage application. From there, the lender will process your loan, and we'll work together to ensure everything is in place for a smooth closing.

How do I know if I’m ready to buy a home?

If you’re financially stable, have a reliable income, and can afford a down payment and monthly mortgage payments, you might be ready. I’ll help you assess your financial readiness and guide you through the process to ensure you’re making the best decision for your future.

What is an FHA loan?

An FHA loan is a government-backed mortgage designed to help first-time homebuyers and those with less-than-perfect credit. It typically requires a lower down payment (as low as 3.5%) and has more flexible credit requirements, making it an excellent option for those who might not qualify for conventional loans.

What is a VA loan, and who qualifies?

A VA loan is a mortgage loan backed by the U.S. Department of Veterans Affairs, designed for military service members, veterans, and certain members of the National Guard and Reserves. It typically requires no down payment or private mortgage insurance (PMI), making it a great option for those who qualify.

What is a USDA loan?

A USDA loan is a government-backed mortgage offered to homebuyers in rural and suburban areas. It requires no down payment and offers competitive interest rates. To qualify, buyers need to meet income and property location requirements, making it a great option for those looking to buy in rural areas.

What is a conventional loan?

A conventional loan is a mortgage that is not insured or backed by the federal government. These loans usually require a higher credit score and a larger down payment than FHA loans, but they come with more flexible terms and potentially lower mortgage insurance costs if you put down at least 20%.

What is a jumbo loan?

A jumbo loan is a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These loans are typically used for luxury or high-value homes and require stricter credit and income qualifications. They also tend to have higher interest rates due to the larger loan amounts.

What is a fixed-rate mortgage?

A fixed-rate mortgage is a loan with an interest rate that stays the same throughout the life of the loan, typically 15, 20, or 30 years. This provides stability and predictable monthly payments, making it a popular choice for many homebuyers.

What is an adjustable-rate mortgage (ARM)?

An adjustable-rate mortgage (ARM) is a type of loan where the interest rate can change periodically based on market conditions. ARMs typically start with lower rates for the first few years and then adjust. While this can offer lower initial payments, it comes with more risk as rates can increase over time.

What is a renovation loan?

A renovation loan, like the FHA 203(k) loan, allows you to finance both the purchase of a home and the cost of repairs or renovations in one loan. This can be a great option if you want to buy a fixer-upper and make improvements to it, as it allows you to finance the project upfront.

"I educate first-time homebuyers so they can make informed decisions"

Said Hamood - Seattle Mortgage Broker - NMLS#1827048

Said Hamood | NMLS #1827048 | Barrett Financial Group, L.L.C. | NMLS #181106 | 275 E Rivulon Blvd, Suite 200, Gilbert, AZ 85297 | TX view complaint policy at www.barrettfinancial.com/texas-complaint | WA MB-181106 | Equal Housing Opportunity | This is not a commitment to lend. *All loans are subject to credit approval. | mlsconsumeraccess.org/EntityDetails.aspx/COMPANY/181106